Midlands Engine Independent Economic Review

Client: Midlands Engine Partnership

The first ever Midlands Engine Independent Economic Review (IER) was published on the 30th April 2020.

SQW led a team of consultants and academics to complete the IER, which was commissioned by the Midlands Engine partnership and formed part of a wider programme of research undertaken by the Midlands Engine Economic Observatory.

The Midlands lies at the heart of the UK, stretching from the Golden Triangle and Western Gateway up to the Northern Powerhouse. With a population of 10.6m people, 816,000 businesses, 5.3m jobs and an annual economic output of more than £233bn, it forms a significant part of the national economy and its long-term success matters to us all.

Historically, the Midlands was at the vanguard of science and industrial innovation. It has become synonymous with globally significant firms and industries operating at the leading edge of advanced technology development and adoption.

The Midlands’ diverse economy has huge potential, but the region faces a number of challenges including a need to improve its productivity performance and respond effectively to the so-called ‘Grand Challenges’.

The primary focus of the IER was on productivity. The research sought to better understand the key factors driving productivity performance in the Midlands, identifying commonalities and economic linkages across the region. It investigated where a genuinely pan-Midlands approach could potentially add most value in terms of addressing strategic challenges and enabling growth opportunities. As well as strengthening the evidence base and influencing policy, the IER has been designed to stimulate debate and discussion.

The main headline findings from the IER are as follows:

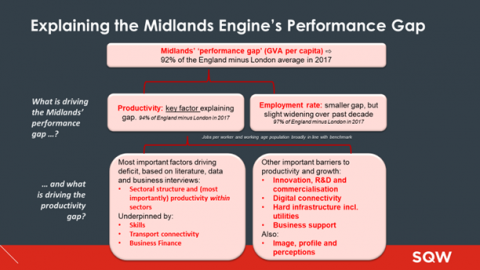

- The Midlands Engine has suffered from a persistent prosperity gap with the rest of the UK (currently at 76% of the UK level or 92% when London is excluded).

- Productivity is the key factor explaining the GVA per capita gap in the Midlands. At the time of writing, productivity in the Midlands was 94% of the England minus London average (or 82% when compared to the rest of England).

- There is considerable spatial variation in productivity performance within the Midlands. Three LEP areas (Coventry and Warwickshire, Greater Birmingham and Solihull, and Leicester and Leicestershire) have higher productivity than the Midlands average and have done so for the last two decades.

- Over time, shifts in the sectoral structure have influenced productivity in the Midlands, with too few jobs in higher productivity sectors. However, productivity performance within sectors (driven by tasks, functions, specialisation and markets) is much more important in explaining the region’s productivity gap.

- According to the evidence gathered for the IER, the most important and common factors holding back productivity and growth across the Midlands are: (i) skills; (ii) infrastructure; (iii) access to growth finance; and (iv) barriers to R&D collaboration, commercialisation and knowledge diffusion/technology adoption.

- The evidence suggests a strong rationale for pan-Midlands effort in terms of: advocacy, identity and promotion; strategic decision-making, case-making and evaluation; joining-up science and innovation agendas; internationalisation; infrastructure development; improving access to growth finance; helping to create the conditions to attract/retain young talent; and addressing key shortages/gaps for the Midlands’ priority sectors.

The main IER Report and supporting technical papers are available to download here: